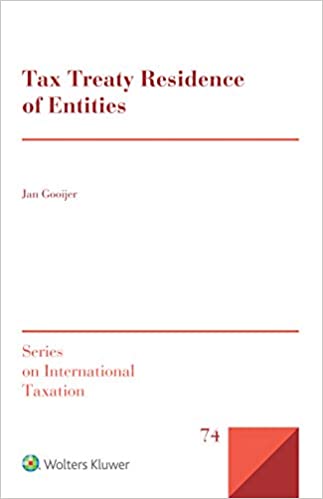

Tax Treaty Residence of Entities

Original price was: $137.75.$48.21Current price is: $48.21.

Order Processing Time

All orders placed on our website are processed within 2-4 business days, from Monday to Friday, 8:00 AM – 6:00 PM Pacific Time (PT). Orders received after our daily cut-off time of 10:00 PM PT will be processed on the next business day. Please note that we do not process orders on weekends or public holidays.

Shipping Methods and Carriers

Zetlly partners exclusively with reputable shipping carriers to ensure timely delivery of your orders. We utilize:

-

FedEx

-

UPS

-

USPS

The choice of carrier is determined by factors such as destination, weight, and delivery timeframe to provide optimal service.

Shipping Rates and Fees

-

Free shipping is provided for all orders over $199.

-

Orders under $199 will incur a flat-rate shipping fee of $7.99.

-

All orders shipped within the United States will be subject to a sales tax charge of 5%.

Estimated Delivery Time

Once shipped, orders typically arrive within 6 to 10 business days. Our delivery times are from Monday to Friday, 8:00 AM – 6:00 PM Pacific Time (PT). Please allow additional time for deliveries to remote or rural locations.

Shipping Restrictions

Zetlly currently ships exclusively within the United States. At present, we do not offer international shipping or deliveries to P.O. boxes or APO/FPO addresses. Orders placed with addresses outside our designated delivery areas will be canceled, and refunds will be processed accordingly.

Tracking Your Order

Upon shipment, customers will receive a confirmation email containing tracking information. You can track your order directly through the provided tracking link or by visiting the carrier’s official website:

Please allow up to 48 hours for tracking information to update in the carrier’s system.

Eligibility for Returns and Exchanges

We accept returns and exchanges within 30 days from the date your order is delivered. Items must be unused, in the original condition, and accompanied by the original packaging and receipt or proof of purchase.

How to Return or Exchange an Item

To initiate a return or exchange, please follow these steps:

-

Contact our customer support at contact@zetlly.com with your order number and reason for return or exchange.

-

Our team will respond within 24 hours to provide detailed instructions, including the specific Return Address for your shipment.

-

Package your item securely and include all original packaging and proof of purchase.

Return shipments should be sent to: Blanq LLC 1201 South Hope Street Apt 2413, Los Angeles, CA 90015, USA

Return Conditions

-

Items must be returned in their original condition, unworn, undamaged, and complete with all original packaging and documentation.

-

Items returned without prior authorization or not meeting the above conditions may not qualify for a refund or exchange.

Return Shipping Costs

Customers are responsible for return shipping costs unless the return is due to our error or a defective product. We recommend using a trackable shipping service to ensure your return reaches us safely.

Non-Returnable Items

The following items cannot be returned:

-

Digital products (e-books or downloadable content)

-

Personalized or customized items

-

Gift cards

Accepted Payment Methods

Zetlly accepts the following secure and widely trusted payment options:

-

PayPal: Easily pay through your PayPal account, benefiting from secure transactions and buyer protection.

-

Stripe: Pay securely using major credit and debit cards including Visa, MasterCard, American Express, and Discover via Stripe’s encrypted payment gateway.

Payment Security

At Zetlly, your security is our utmost priority. We utilize advanced encryption technologies and robust security protocols provided by PayPal and Stripe. All payment information entered on our site is encrypted using Secure Socket Layer (SSL) technology, ensuring your financial information remains private and secure throughout the transaction process.

Zetlly does not store any credit card or sensitive financial information directly on our servers, further enhancing the security and protection of your personal data.

Payment Process and Confirmation

Upon placing an order, your chosen payment method (PayPal or Stripe) will immediately process the transaction. You will receive an automated confirmation email shortly after your payment has been successfully completed, detailing your transaction and order summary.

Please retain this confirmation email for your records and reference in case of any inquiries or disputes.

It is of great importance to be able to determine who or what is considered ‘resident’ within the meaning of tax treaty provisions. However, the concept of residence has never been fundamentally adjusted to current circumstances in which technological developments make it possible for corporations to explore the wide gap between their actual business operations and the ‘legalistic’ requirements for corporate residence. In this study of the OECD Model Tax Convention -the basis for most tax treaties -the author develops a clear understanding of the content of the residence concept as regards entities and proposes solutions to current problems, finishing with his own thoroughgoing definition. In seeking a definition of the term ‘resident’ that covers all uses in treaties, the analysis draws on, in addition to the current and earlier iterations of the OECD Model Law itself, such elements as the following: domestic law meaning of residence in the tax law of France, Germany, the Netherlands, the United Kingdom and the United States; Articles 31 and 32 of the Vienna Convention on the Law of Treaties; historical documents that uncover the ordinary meaning of treaty terms; tax treaty case law and court decisions; and fiscal, tax and legal scholarship surrounding the concept of residence for taxation purposes. The analysis includes a comprehensive description of tiebreaker rules, various perspectives on ‘place of effective management’ and policy considerations as to the further development of the treatment of entities under double tax conventions. Given the inordinate importance of the definition of ‘resident’, the differences in interpretation to which the current definition gives rise and the economic developments that call for an evaluation of the provision, this thorough examination of the treaty rules on residence of entities will be welcomed by tax lawyers, corporate counsel and policymakers and academics concerned with tax law. The author’s guidance on the concept of residence for tax purposes and his original proposals for reform will prove of great practical value for tax practitioners.Product details Simultaneous Publisher: Kluwer Law International (September 13, 2019) Publication Date: September 13, 2019

Related products

Ebook New zetlly

Adam Smith: A Moral Philosopher and His Political Economy (Great Thinkers in Economics)

Ebook New zetlly

Ebook New zetlly

The Illustrated Network: How TCP/IP Works in a Modern Network

Ebook New zetlly

Art Fundamentals Theory and Practice 12th dition by Otto Ocvirk

Ebook New zetlly